Canada has a strong AI industry with excellence in research and several prominent AI startups. Recent federal government initiatives — including a five-year program to expand domestic compute capacity, upgrades to public research infrastructure, and the C$300-million AI Compute Access Fund launched in March 2025 — are designed to improve affordable access to graphic processing units (GPUs) and support commercialization across firms and research organizations.

AI is now emerging not only as a driver of domestic innovation and productivity, but also as a tradable asset. Canadian AI-driven startups export AI models, generative tools, and autonomous agents. AI solutions are also an indirect export, used in the production of Canada’s manufacturing, agricultural, mining, and services exports. At the same time, Canadian firms also import essential AI inputs (such as ICT equipment, compute infrastructure, specialized services, skilled labour, and data) that underpin AI development and deployment.

However, there is still limited policy thinking around Canada’s opportunities to grow “trade in AI,” here broadly defined as trade by AI-driven businesses (such as AI startups, typically in computer services) and trade in services and goods industries in which firms use AI intensively, where a large share of firms use AI. There is also little thinking to date on trade policies that could promote AI exports in particular. This paper — the first in a three-part series — seeks to fill that gap by examining how AI already features in Canada’s trade performance and promoting thinking on Canadian policies that could grow Canada’s trade in AI.

This first paper proposes a working definition of “trade in AI” and examines the scale and characteristics of Canada’s AI-related trade using industry, firm-level, and value-chain evidence. Two subsequent papers will discuss how Canada’s trade policy, especially in the Indo-Pacific, could promote greater trade in AI.

Indo-Pacific markets are still small but increasingly important destinations for Canada’s AI-intensive exports. In 2023, the Indo-Pacific absorbed 5.4 per cent of Canada’s total exports of AI-intensive services, up from 4.8 per cent in 2014. North American markets make up 62 per cent (U.S., 61 per cent; Mexico, one per cent) of the total. The share of exports to the Indo-Pacific has grown, especially in Canada’s computer-services exports, from 3.3 per cent to six per cent from 2014-23, while North America’s share has declined from 78 per cent to 68 per cent.

Key Takeaways

This paper identifies several reasons why artificial intelligence (AI) policies are both important and timely for advancing Canada’s trade. In particular:

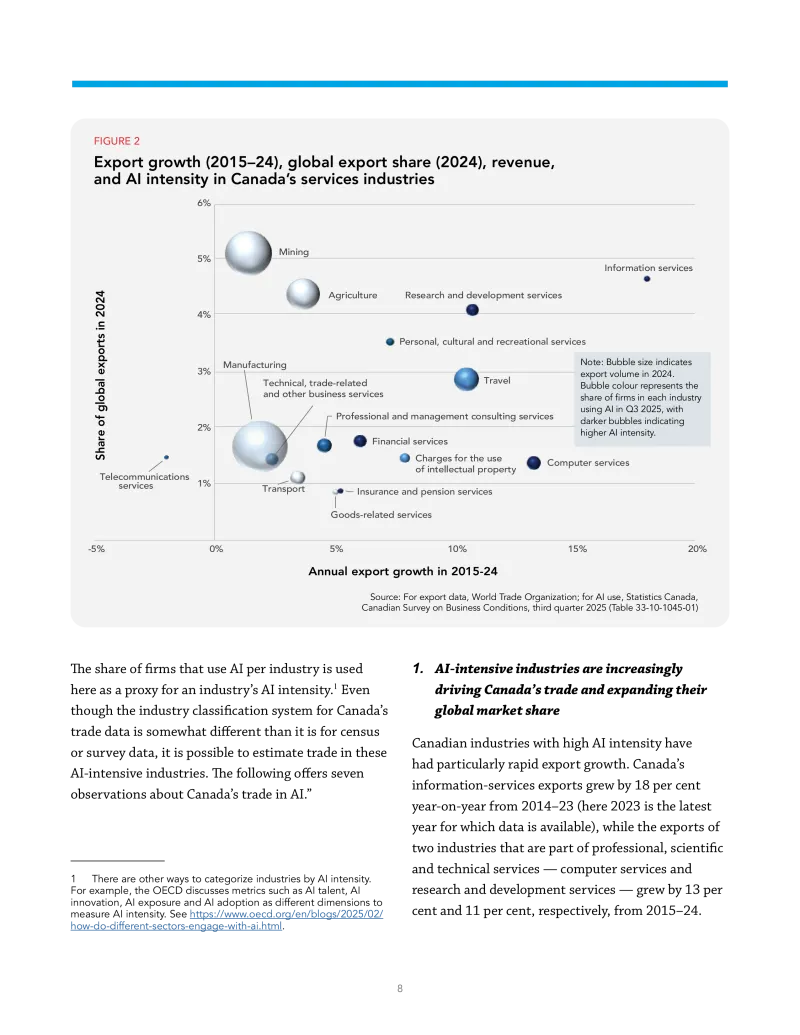

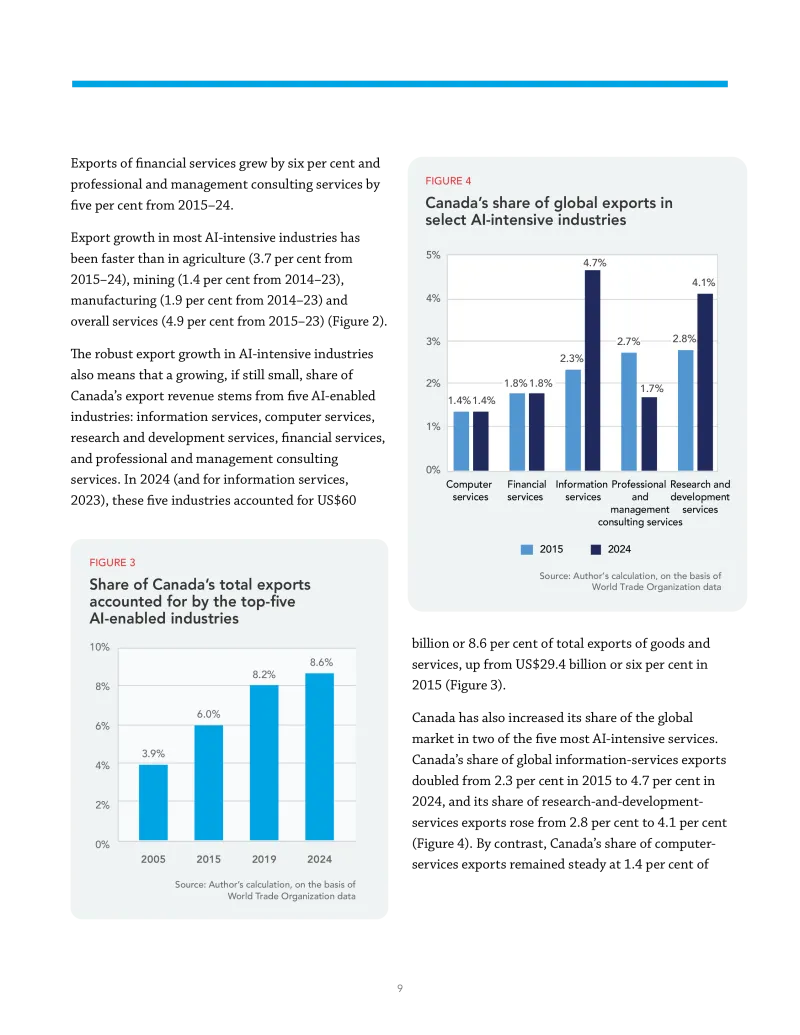

- Canadian industries that have the highest AI intensity (highest share of firms using AI, including information services, computer services, research and development, financial services and professional services) all grew faster than Canada’s goods exports over the last 10 years. These industries now make up a growing share of Canada’s total exports, generating 8.6 per cent of all export revenue in 2024, up from six per cent in 2015.

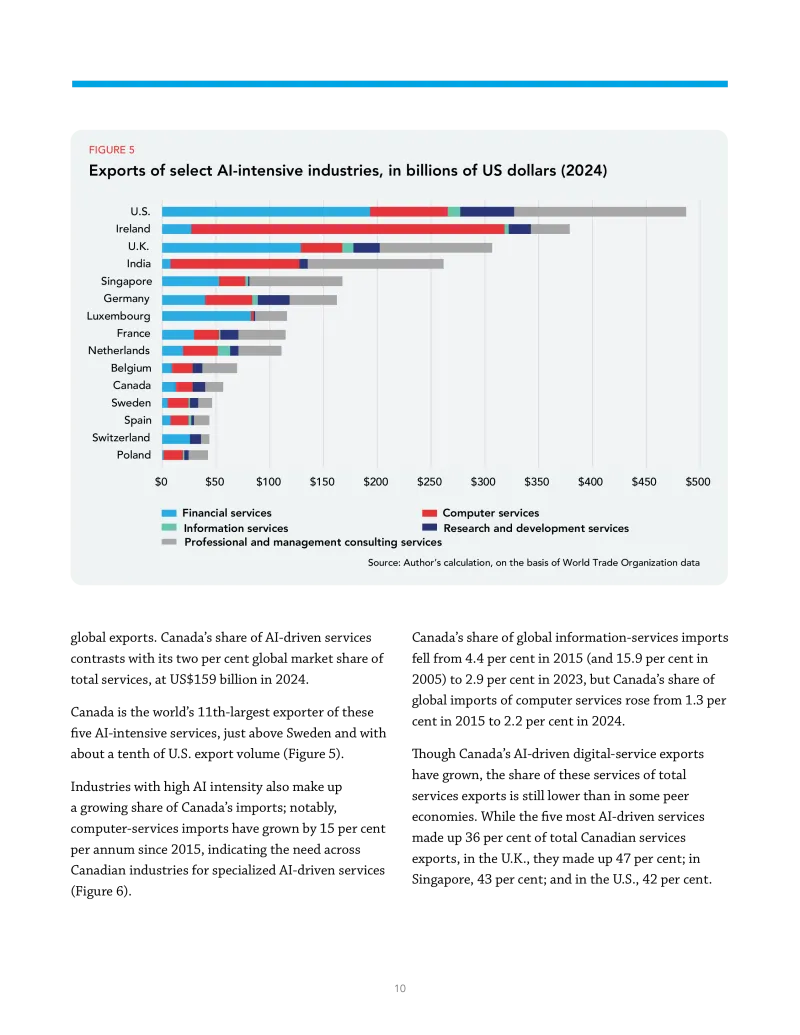

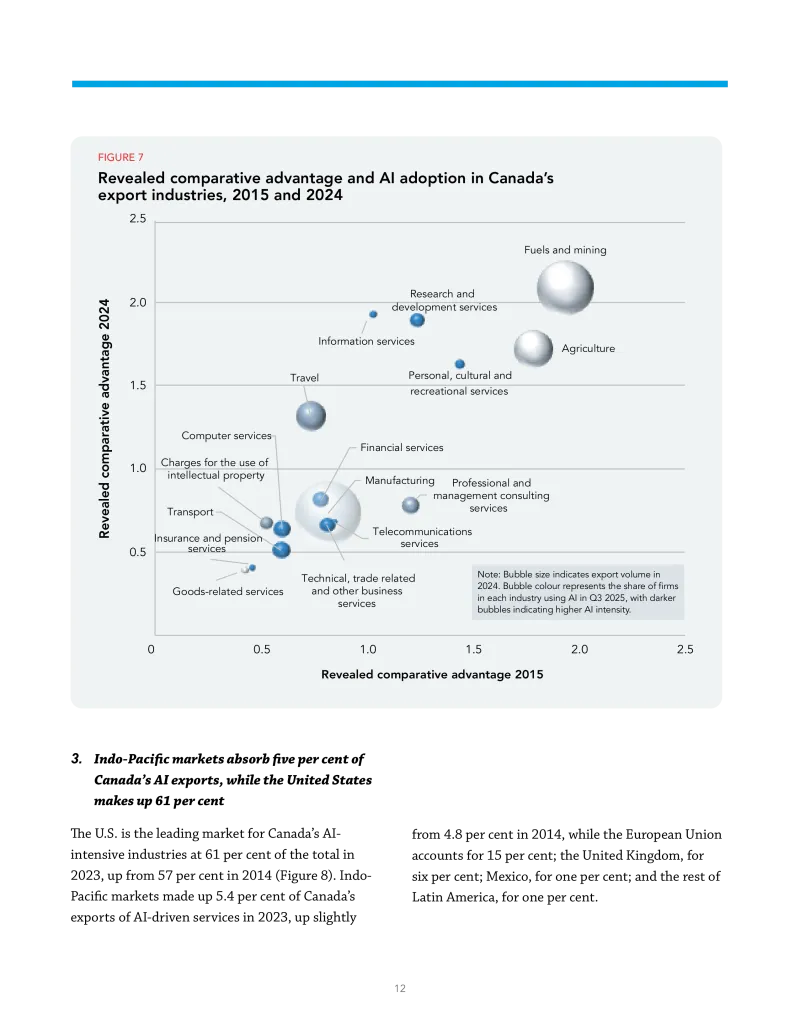

- Canada is the world’s 11th-largest exporter of these AI-intensive services. Canada’s share of information-services exports has doubled from 2.3 per cent of world exports in 2015 to 4.7 per cent in 2024, and research-and-development services exports have grown from 2.8 per cent to 4.1 per cent. Canada has a revealed comparative advantage in these AI-intensive services.

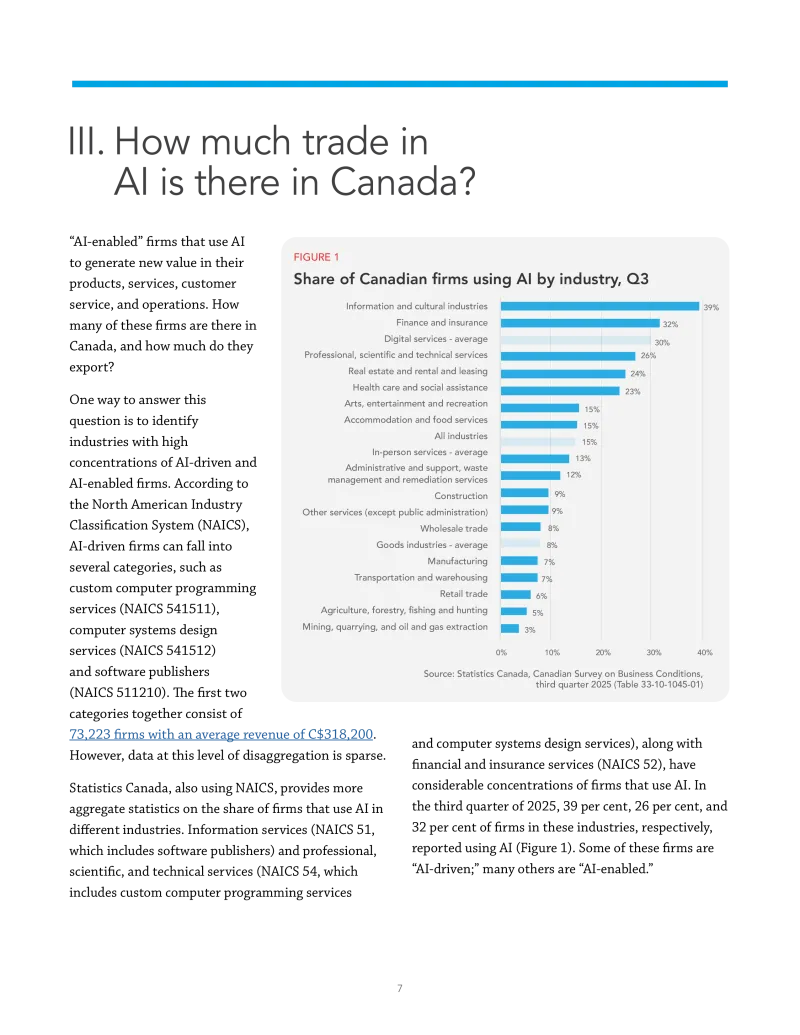

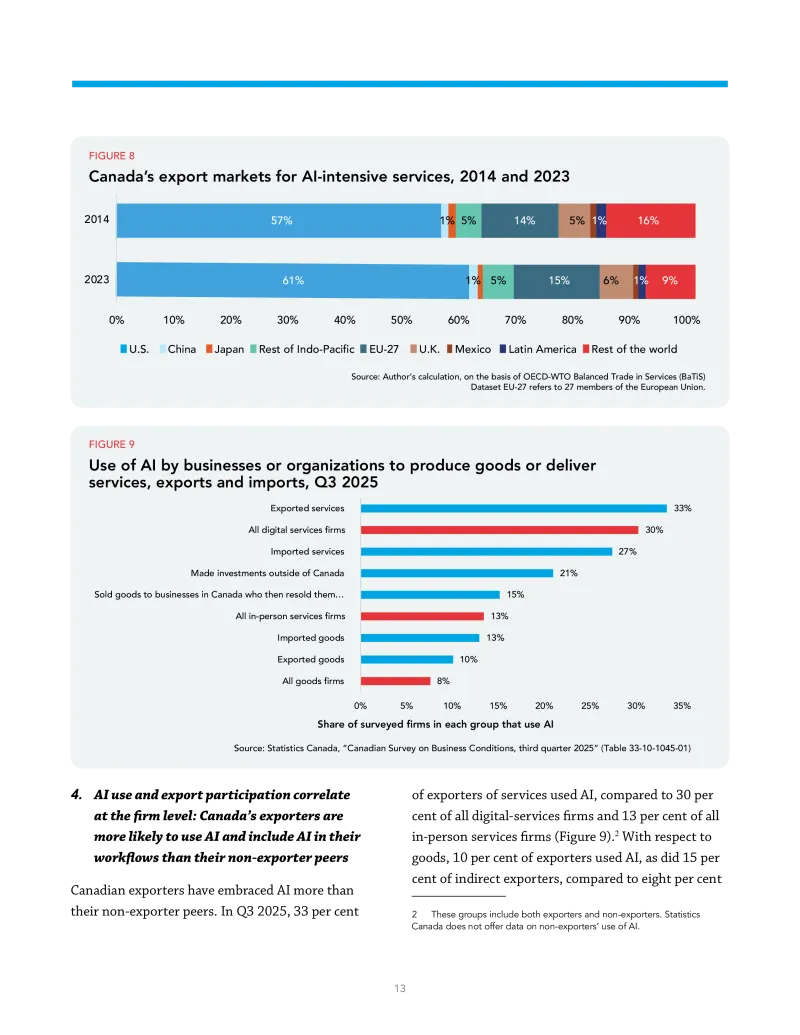

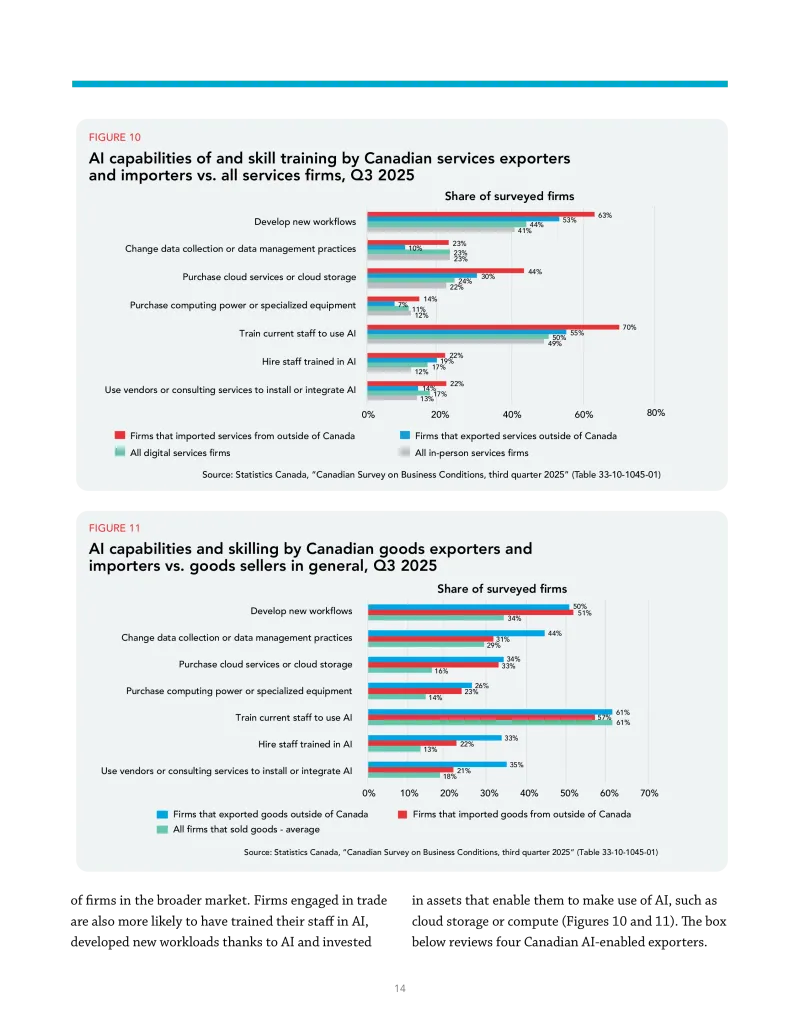

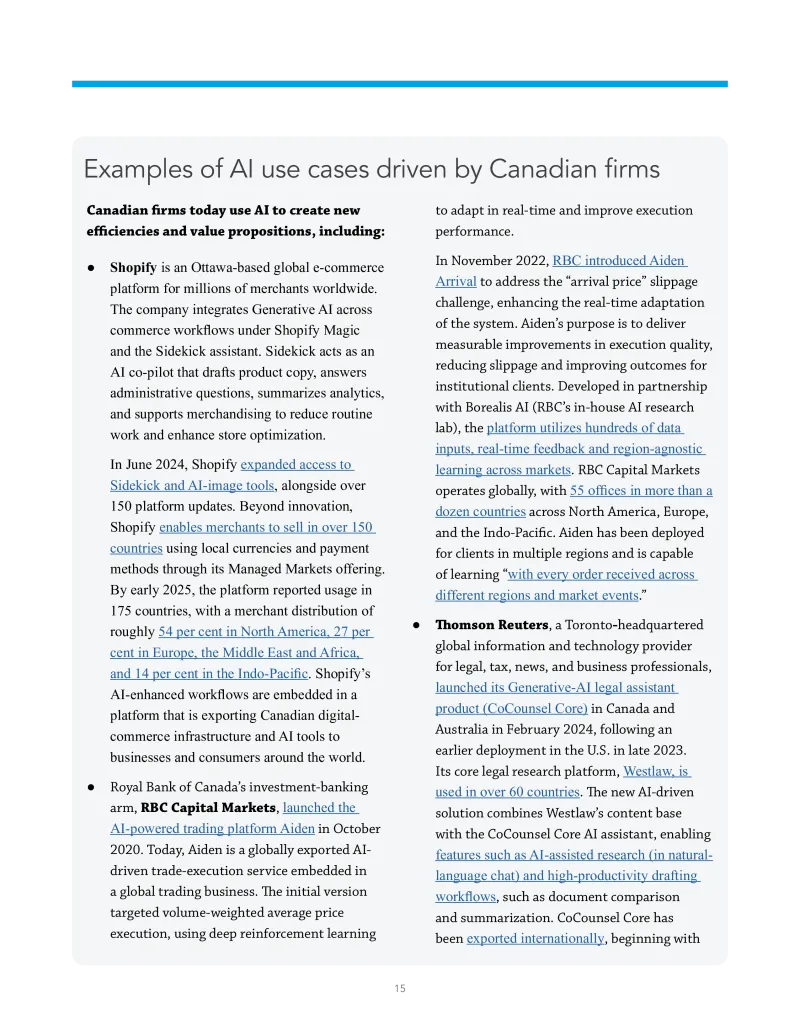

- At the firm level, Canadian exporters are more likely to use AI than non-exporters. In the third quarter of 2025, 33 per cent of services exporters used AI, compared to 30 per cent of all digital services firms and 13 per cent of all in-person services firms. Of goods-producing firms, 10 per cent of exporters used AI, as did 15 per cent of indirect exporters, compared to eight per cent of goods sellers overall.

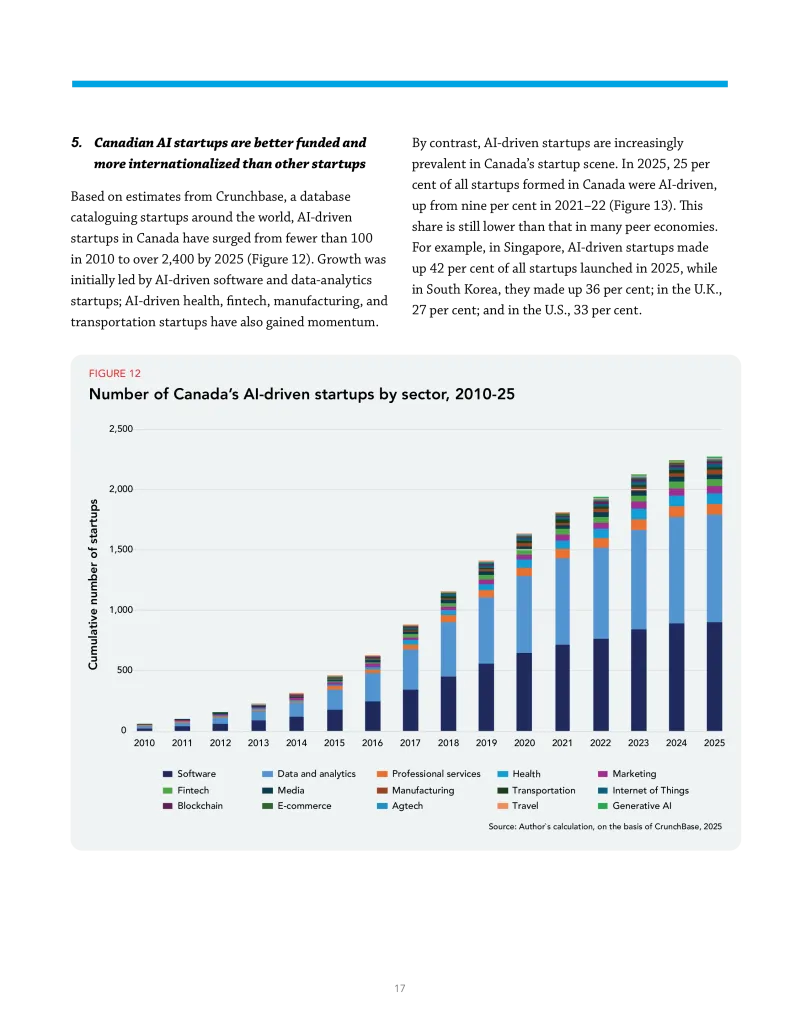

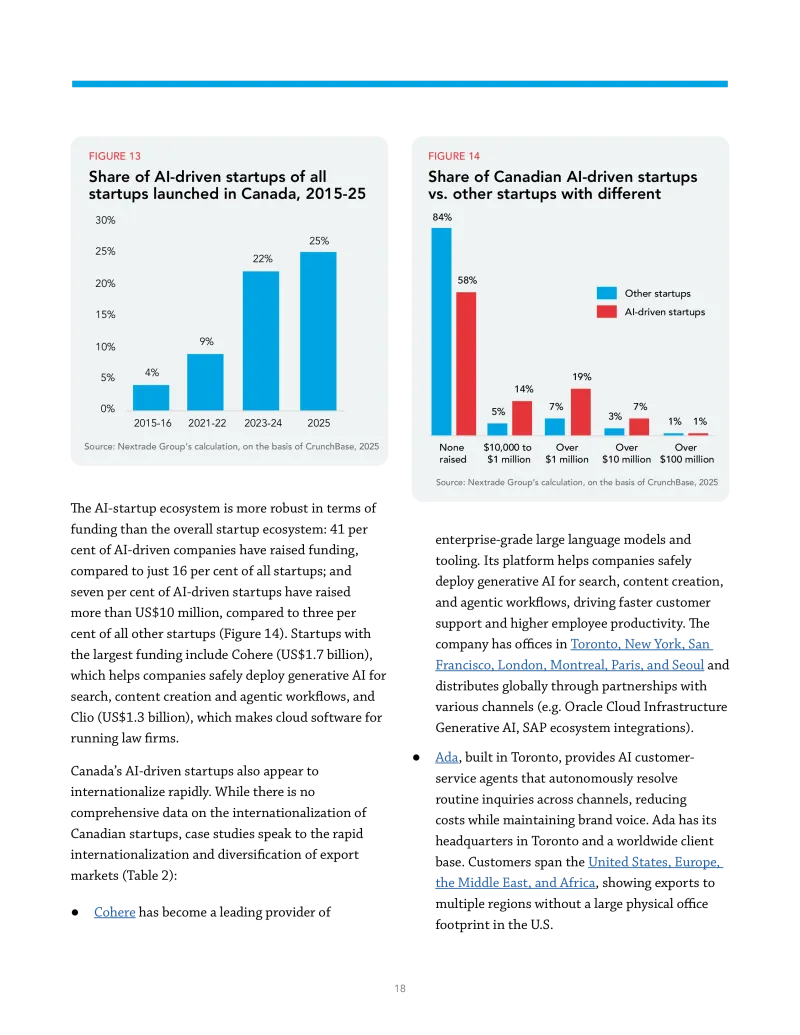

- Canada’s AI-driven startups are better funded than startups in general, with companies like Cohere, Ada, BenchSci, and Waabi scaling quickly to offer their services in the U.S., Indo-Pacific, and European markets.

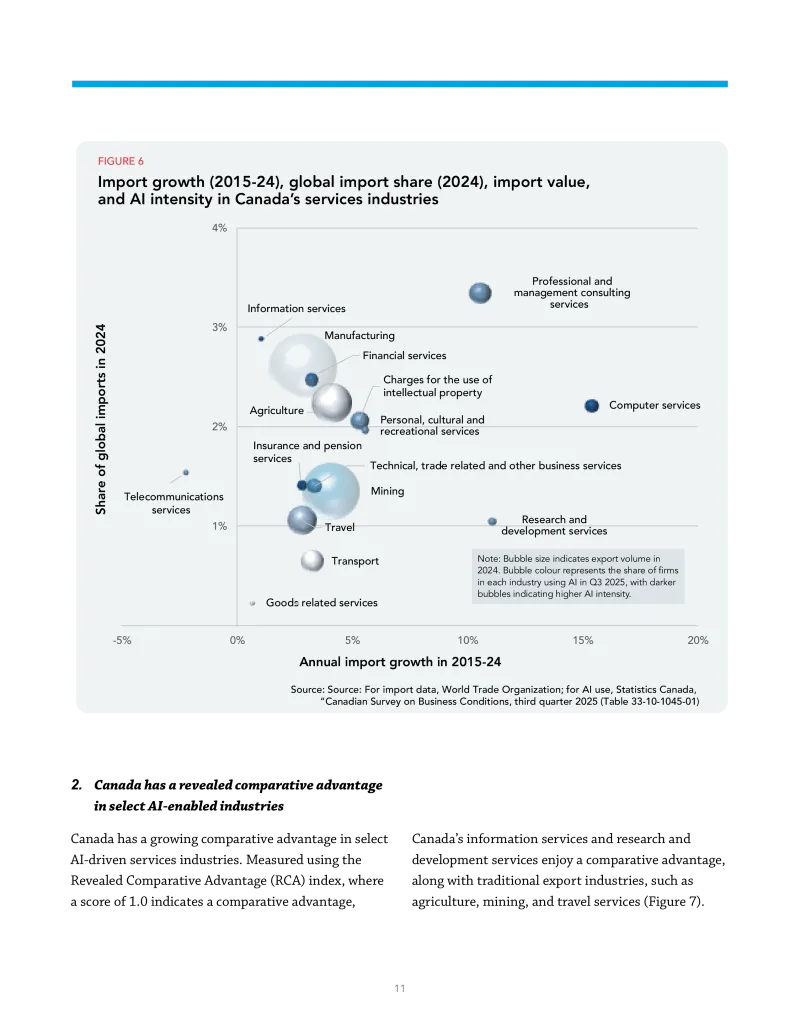

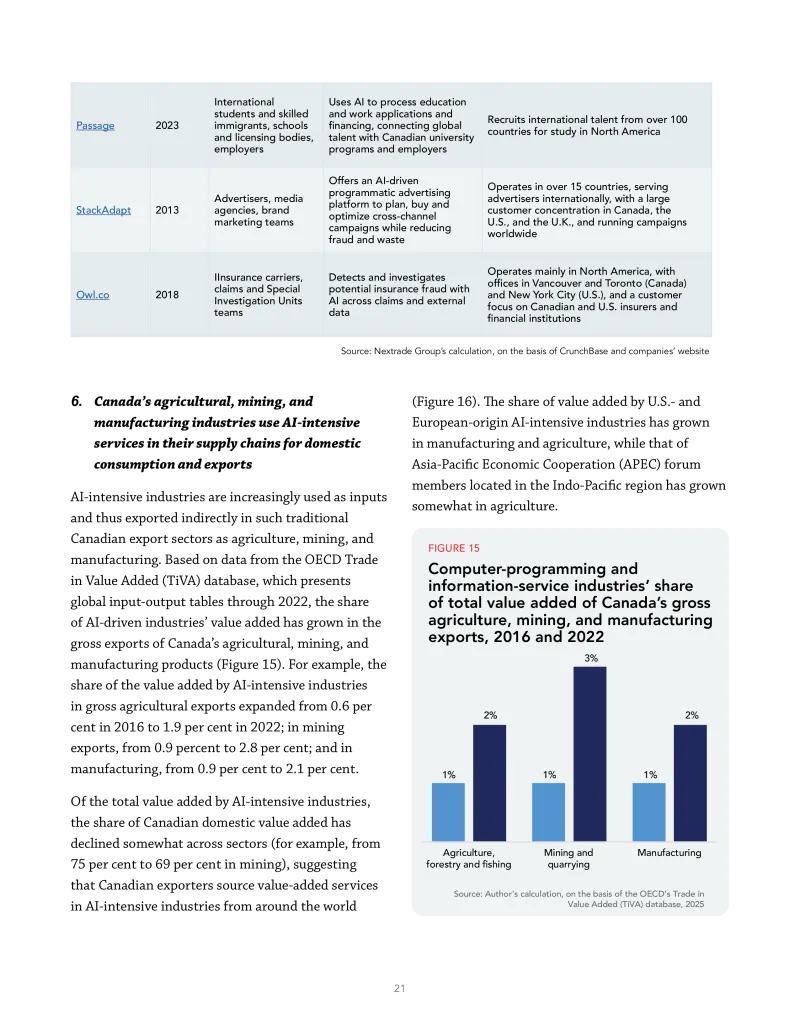

- AI-driven services have become more prominent as inputs into Canadian companies’ supply chains and final products destined for export. For example, the AI-intensive industries’ share of the value added in gross mining exports has expanded from 0.9 per cent in 2016 to 2.8 per cent in 2022 (the latest year for which data is available); in manufacturing, from 0.9 per cent to 2.1 per cent; and in financial services, from 3.5 per cent to 6.6 per cent. Most of these AI intensive inputs are domestic, though a growing share is of foreign origin.

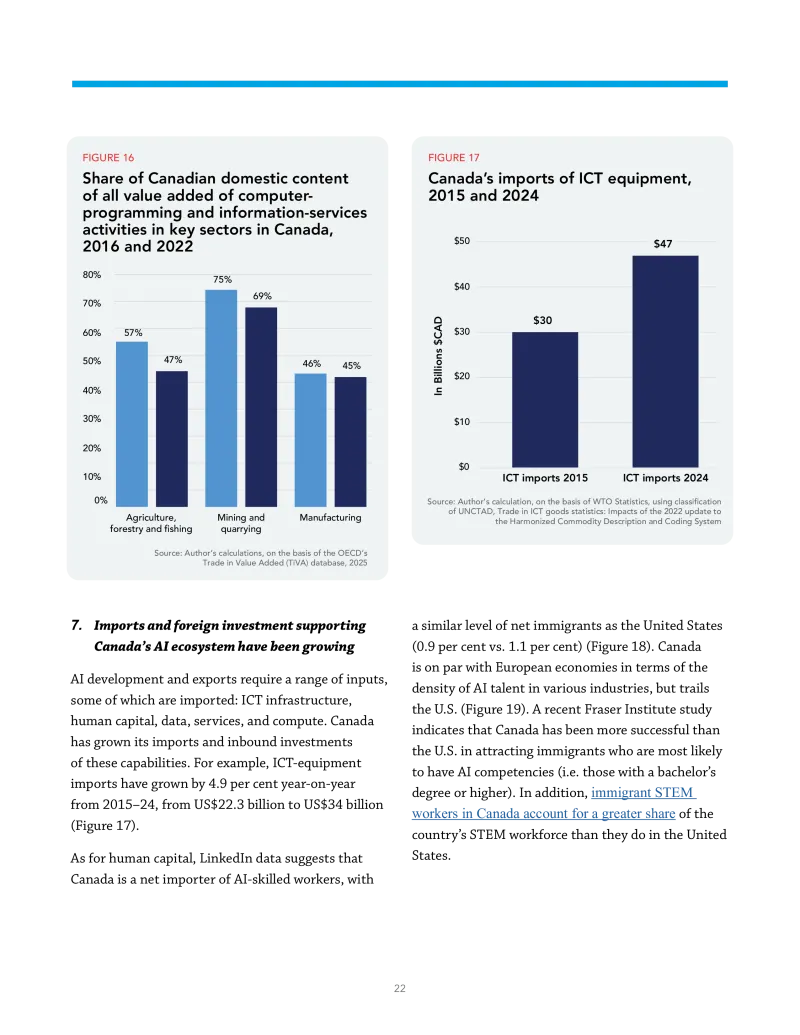

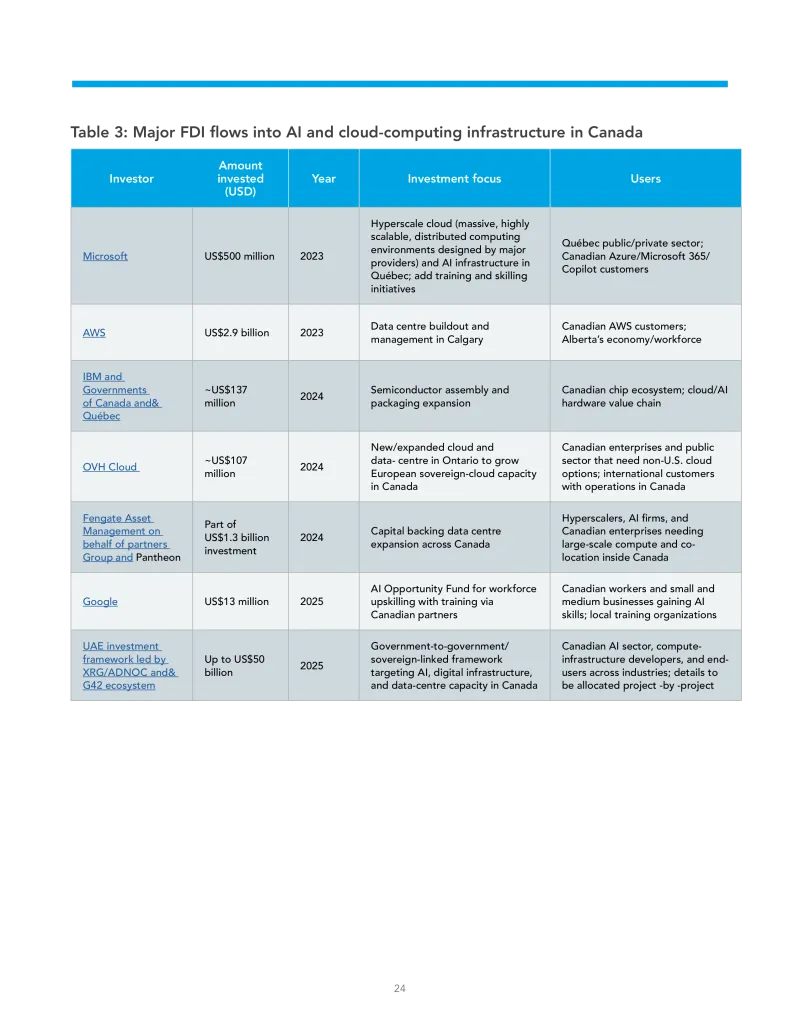

- Imports of various AI capabilities for Canada’s AI development — such as information and communication technology (ICT) equipment, human capital and foreign direct investment (FDI) in cloud, compute, and AI labs — have been growing robustly in recent years, supporting Canada’s AI development and exports of AI.

Read the full report below, or download a copy above.